Hadwick Town Hall Explains Insurance Market Strain

Speakers outlined wildfire risk, state reforms, and FAIR Plan limits.

7 min read

DISTRICT 1 — Assemblywoman Heather Hadwick hosted a virtual insurance town hall Tuesday evening, bringing together representatives from the insurance industry, the California Department of Insurance, and the California FAIR Plan to explain why many residents are seeing higher premiums, fewer coverage options, or a move into last-resort coverage.

Hadwick’s office announced the event in May in response to rising insurance costs and low availability, which it described as one of the most pressing concerns facing Californians. In the announcement, Hadwick said affordability had been the top concern in a constituent survey, with insurance “as a close second,” adding, “These issues go hand in hand. California is a very expensive place to live, and people can’t afford the rising cost of insurance.”

Hadwick opened the meeting by noting the size and geography of Assembly District 1, which includes 11 mostly rural and forested counties: Alpine, Amador, El Dorado, Lassen, Modoc, Nevada, Placer, Plumas, Shasta, Sierra, and Siskiyou. She said her office had received more than 1,000 responses to a survey, and insurance ranked at the top of concerns for the district.

“We wanted to get you guys in the room with the experts,” Hadwick said. The town hall featured Seren Taylor, vice president of the Personal Insurance Federation of California; Durriya Syed of the California Department of Insurance; and Kyle Belvill, vice president of product and underwriting for the California FAIR Plan.

The speakers described California’s home insurance market as a system built around a voluntary market, state regulation, and a last-resort safety net. In the voluntary market, private insurers decide where to write policies, while their rates and forms are reviewed by the California Department of Insurance. When homeowners cannot find coverage in the regular market, they may turn to the California FAIR Plan, which provides basic property coverage but is not designed to replace a full homeowners policy.

Taylor, speaking from the industry perspective, said the current crisis has been driven by two major forces: catastrophic wildfire losses and the rising cost of rebuilding homes. He said California has experienced many of the costliest wildfires in history, including the Camp Fire, the Tubbs Fire, and the more recent Palisades and Eaton fires, which he said are expected to produce tens of billions of dollars in insured losses.

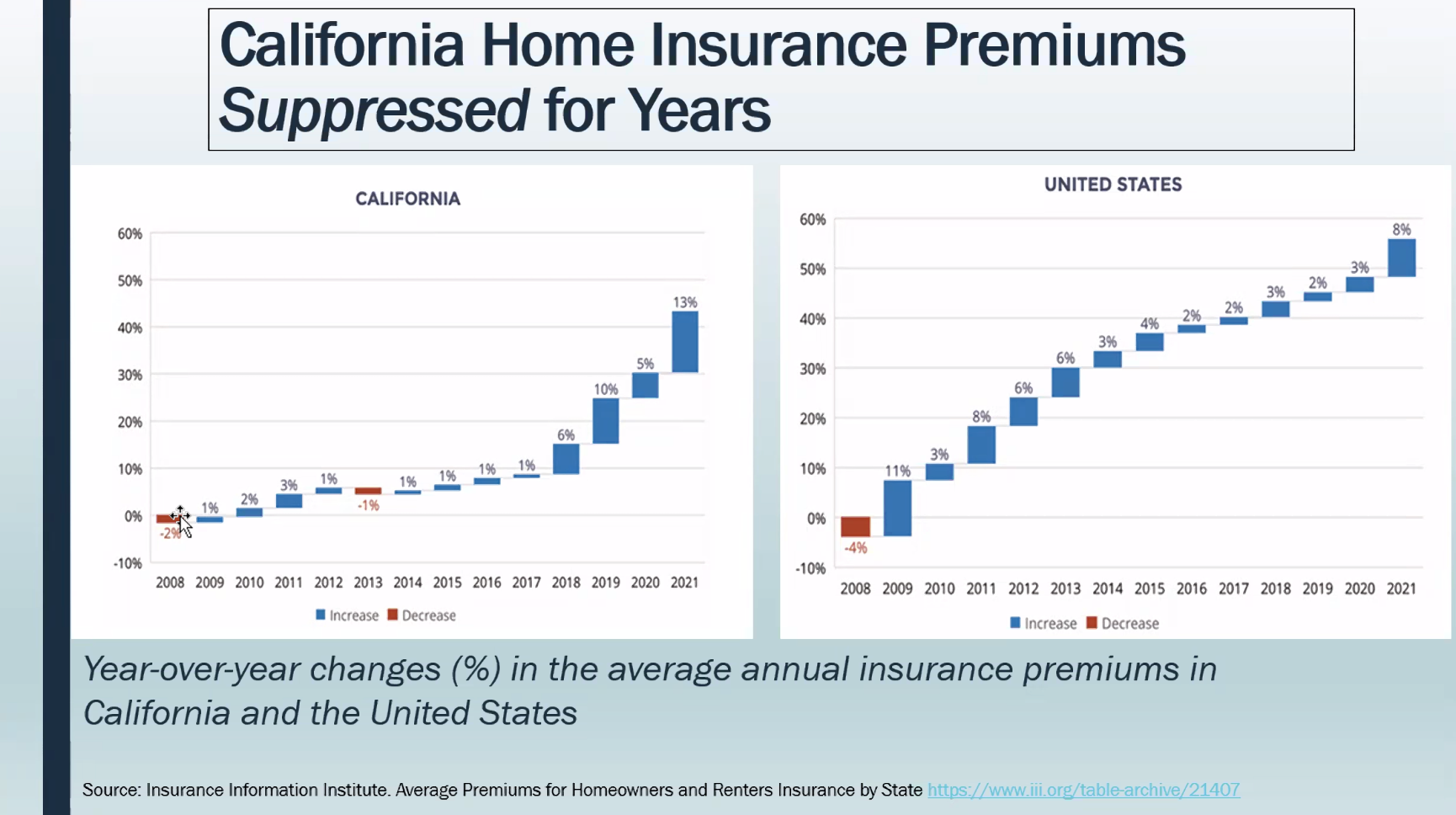

A slide shared by Taylor demonstrating suppression of California home insurance premium increases when compared to national rates.

Taylor also said rebuilding costs have risen sharply since the COVID period. According to his presentation, residential construction goods, services, and materials rose by nearly 35% in two years, while residential construction costs increased 64% over a decade.

The result, Taylor said, is a market in which premiums rose quickly after years in which companies were not able, in his view, to price policies to match the risk. He argued California’s previous rate system relied too heavily on past losses and did not allow insurers to fully account for growing wildfire risk until losses had already occurred.

Taylor said California’s recent insurance reforms are intended to move the market toward forward-looking risk analysis. Under the state’s Sustainable Insurance Strategy, insurers can use catastrophe models and include reinsurance costs in rate filings, while also being required to write more policies in wildfire-distressed areas.

A major goal, Taylor said, is to bring people back from the FAIR Plan into the admitted market, a process often described as “depopulating” the FAIR Plan. He said about nine companies had already made filings under the Sustainable Insurance Strategy, representing more than one-third of the market.

Taylor also emphasized wildfire mitigation. He pointed to measures such as ember- and flame-resistant vents, a Class A fire-rated roof, noncombustible gutters, six inches of noncombustible vertical clearance at the base of exterior walls, and a five-foot ember-resistant zone around a home. More extensive work can include wildfire-resistant decks, dual-pane or tempered-glass windows, and covered gutters.

Syed, speaking for the California Department of Insurance, described the market pressures in similar terms, including more severe climate-related events, inflation, rising reinsurance costs, and fewer coverage options in some areas. She said the department’s work is centered on two major initiatives: Safer from Wildfires and the Sustainable Insurance Strategy.

Safer from Wildfires focuses on mitigation at three levels: the structure itself, the immediate surroundings, and the broader community. Syed said the program is designed to reduce risk while also requiring insurers to recognize mitigation work through discounts and greater transparency.

For individual homes, Syed mentioned items such as a Class A roof, enclosed eaves, fire-resistant vents, multi-pane windows, and noncombustible material at the bottom of exterior walls. For the area around a home, she pointed to clearing vegetation and debris under decks, removing movable combustible materials, and addressing nearby sheds or outbuildings.

The third layer is community mitigation. Syed highlighted Firewise USA and Fire Risk Reduction Community designations, saying the community approach can help residents work together, pursue grants, and assist neighbors who may have limited income or limited ability to complete defensible-space work on their own.

Syed also urged residents to understand the difference between non-renewal and cancellation. A non-renewal generally gives a homeowner time to shop for new coverage before a policy ends. A cancellation may occur for reasons such as nonpayment of premiums or a serious hazard on the property, and Syed strongly urged residents to pay premiums on time.

She said homeowners can ask their insurer for their wildfire risk score at several points: when applying for a new policy, before renewal, before non-renewal, and after completing mitigation work. If a homeowner believes a rate or risk score is wrong, Syed encouraged contacting the Department of Insurance.

Syed said 29 counties are in distressed insurance areas. She said six companies had committed to growing in California under the Sustainable Insurance Strategy, with more expected to follow, and noted that some filings will take effect later in the year.

She also directed residents to the Department of Insurance's consumer tools, including a home insurance finder designed to identify companies that write policies in higher-risk areas. If coverage cannot be found in the admitted market , Syed said non-admitted or surplus-line options may exist, but she cautioned consumers to be careful and use department resources.

Belvill closed the presentations with an overview of the California FAIR Plan. He said the FAIR Plan is California’s insurer of last resort, providing basic property coverage regardless of a property’s fire risk. He stressed that the FAIR Plan is not a state agency, is not funded by taxpayers, and is not intended to compete with regular insurers.

The FAIR Plan was created by statute in 1968 following the riots and brush fires of the 1960s. Belvill said the plan functions as a temporary safety net for property owners who cannot find coverage in the voluntary market.

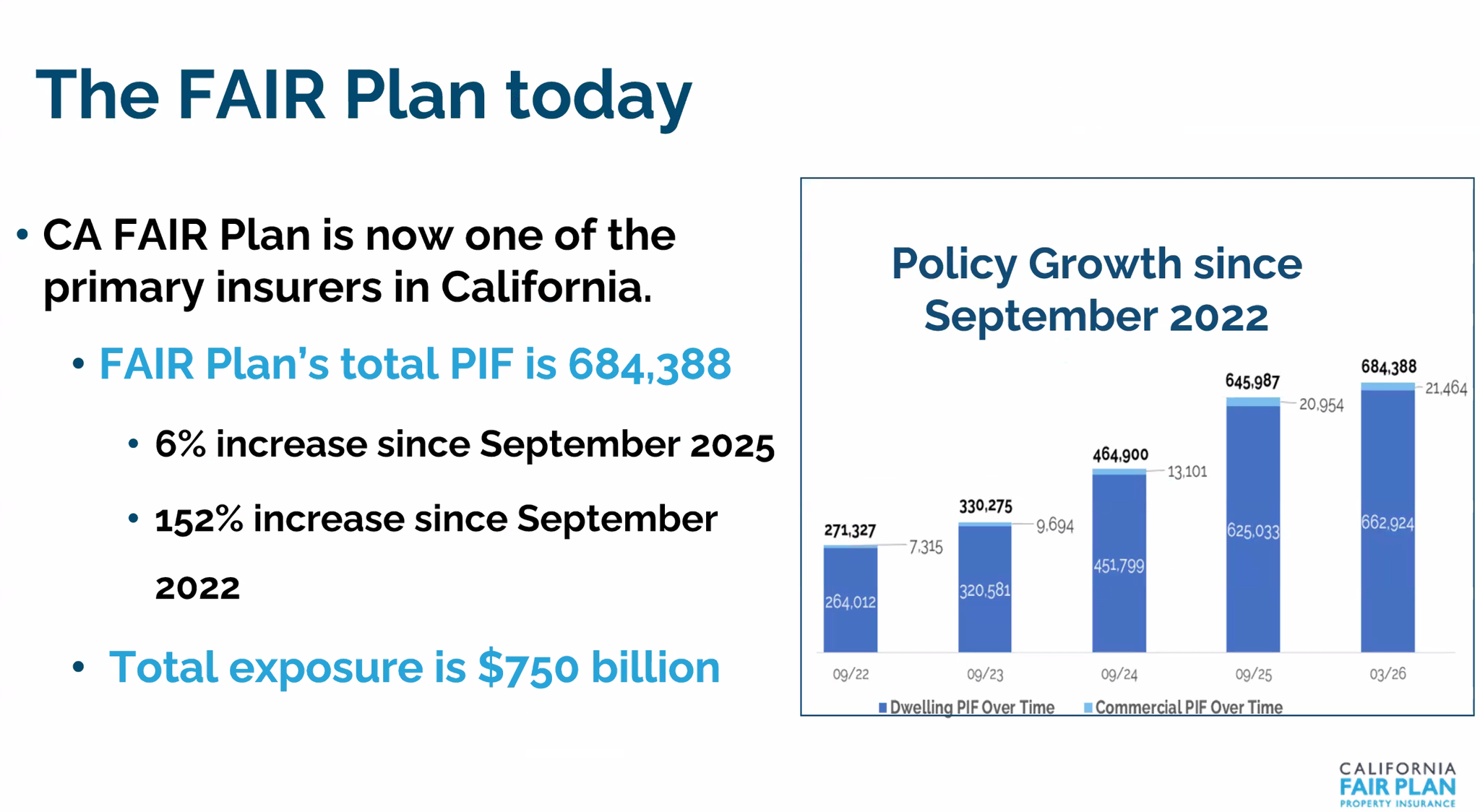

A slide shared by Belvill showing growth in the number of California FAIR Plan policies from 2022 to 2026.

Belvill said the FAIR Plan had 684,000 policies in force through the end of March, a 6% increase since September 2025 and a 152% increase since September 2022. He said the plan’s total exposure had grown to $750 billion.

The FAIR Plan offers dwelling coverage for owner-occupied, tenant-occupied, and certain multi-family properties of up to four units, as well as personal property coverage for renters and condominium owners. It also offers commercial coverage for business-owned buildings, farms, wineries, offices, and larger habitational properties, and it can provide earthquake coverage through the California Earthquake Authority.

Belvill emphasized that the FAIR Plan does not offer a standard homeowners policy. It does not cover some major parts of a typical homeowners policy, including water damage, theft, and liability coverage. Homeowners who use the FAIR Plan often need a separate Difference in Conditions policy to add coverage closer to a comprehensive homeowners policy.

Like other presenters, Belvill discussed wildfire-hardening discounts. He said the FAIR Plan offers five discounts tied to protecting the structure and five tied to protecting the immediate surroundings, with an additional property-level completion discount when all 10 are met. He also said some communities may qualify for community-level discounts through Firewise USA or Fire Risk Reduction Community participation.

Belvill said FAIR Plan customers can submit claims online at any time or by phone during regular business hours. He also said the plan has recently updated dwelling policy language, added recurring payment options for three- and 11-payment plans, and plans to begin offering optional replacement-cost coverage for mobile and manufactured homes on October 15, the same date as a dwelling policy rate change.

At the end of the meeting, Hadwick’s staff said they were tracking questions submitted during the event, several of which emphasized reliance on the FAIR plan and general dissatisfaction with insurance options, and would follow up with attendees. Staff also said the meeting recording would be circulated.